🧠 QuantHQ Tutorial: Regime Detection API for Smarter Trading Strategies

Welcome to this hands-on walkthrough using QuantHQ's Regime Detection API — a powerful tool that helps you identify market regimes using machine learning.

In this tutorial, we’ll show how to:

Detect bullish, bearish, or neutral market regimes in real-time

Use this signal to dynamically adjust trading strategies

Backtest regime-aware logic using PyFolio and Pandas

Pull market data using yfinance

Integrate QuantHQ's API into your own research pipeline

Whether you're a retail quant, macro trader, or hedge fund analyst, this tutorial will give you a simple framework to enhance your models using modern signal intelligence.

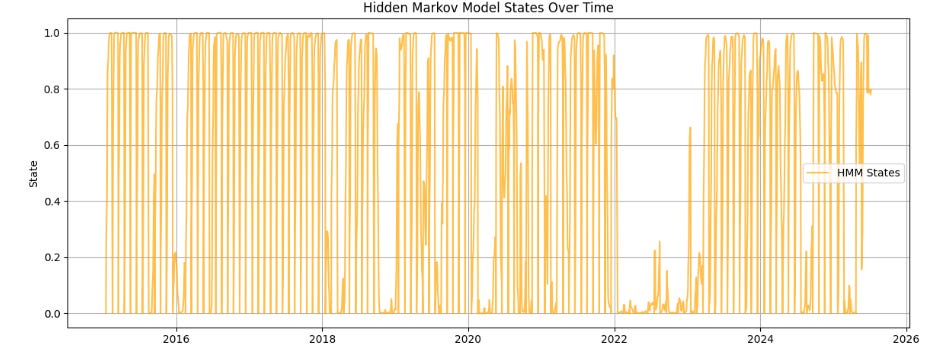

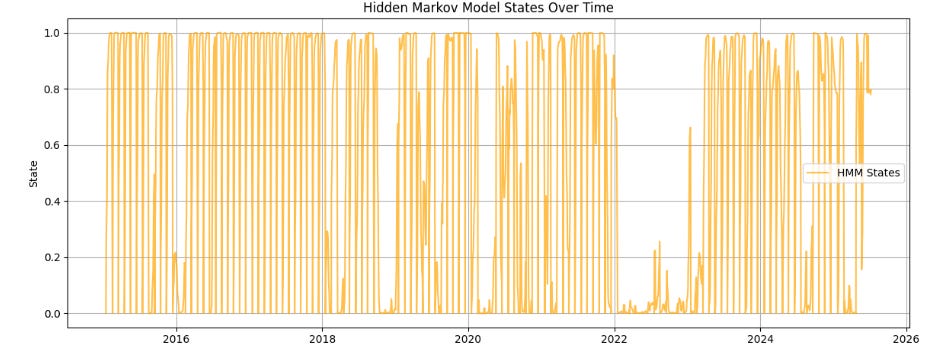

🔌 QuantHQ API Integration: Regime Detection via HMM

This code connects to the QuantHQ Hidden Markov Model (HMM) Regime Detection API and visualizes market regime shifts over time.

🧾 What It Does:

Sends a POST request to QuantHQ’s

/api/hmmendpointAuthenticates using your API key (

Bearertoken in header)Requests regime data for

QQQfrom 2015-01-15 to 2025-07-09Parses the JSON response and extracts relevant fields:

id,symbol,date, and regime signal (rhoT)

Loads the data into a pandas DataFrame

Converts:

date→datetimesignal→ numeric HMM regime values (e.g., 0 = bear, 1 = neutral, 2 = bull)

Calls the

plot_hmm_state_transitions(df)function to create a clean visual of how market regimes evolve over time

import requests

import pandas as pd

# API call setup

url = "https://quanthq.io/api/hmm"

api_key = "YOUR_API_KEY" # Replace with your actual key

headers = {

"Authorization": f"Bearer {api_key}",

"Content-Type": "application/json"

}

payload = {

"symbol": "QQQ",

"startDate": "2015-01-15",

"endDate": '2025-07-09'

}

response = requests.post(url, headers=headers, json=payload)

if response.status_code == 200:

raw_data = response.json()

# Extract just the fields you care about from the nested 'data' object

# Example if the API returns {"data": [...actual records...]}

records_raw = raw_data.get("data", [])

records = []

for item in records_raw:

records.append({

"id": item.get("id"),

"symbol": item.get("symbol"),

"date": item.get("date"),

"signal": item.get("rhoT")

})

# Convert to DataFrame

df = pd.DataFrame(records)

# Clean data types

df["date"] = pd.to_datetime(df["date"])

df["signal"] = pd.to_numeric(df["signal"], errors="coerce")

print(df.head()) # optional preview

# Plot HMM state transitions

plot_hmm_state_transitions(df)

else:

print(f"API request failed with status {response.status_code}: {response.text}")

📊 Output:

A preview of the processed DataFrame

A time series plot of the regime signal, ideal for identifying trends, volatility clusters, or structural breaks in the market

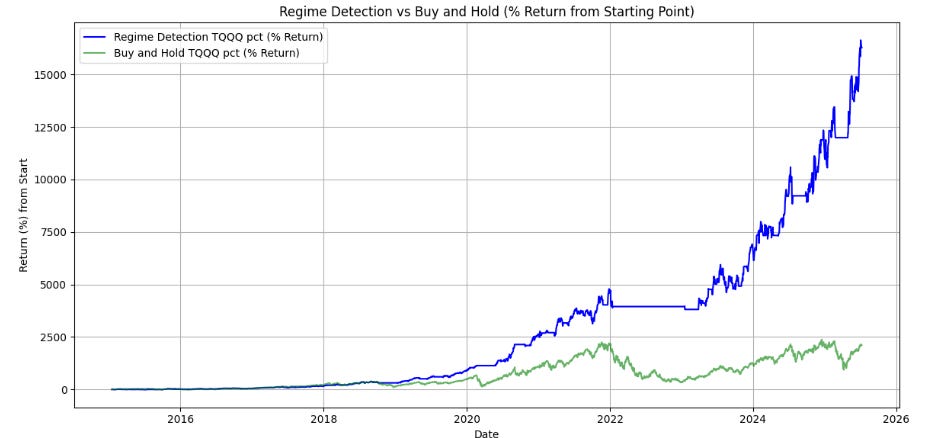

📊 Explosive Backtest Results: TQQQ Strategy Using QQQ Regime Detection

What happens when you apply QuantHQ’s regime detection signal (trained on QQQ) to a leveraged ETF like TQQQ?

✅ Total return: +16,283.12% (Jan 2015–July 2025, simulated)

This isn’t magic — it’s a simple regime-aware overlay. We didn’t tweak parameters, curve-fit, or optimize for hindsight. We just followed this logic:

df['position'] = np.where(df['signal'] > 0.6, 1, 0)When the Hidden Markov Model (HMM) gives a strong bull signal, we take a position. Otherwise, we sit in cash.

💡 Strategy Overview

Signal source: QQQ (NASDAQ-100)

Traded asset: TQQQ (3x leveraged version of QQQ)

Approach: Only enter when bull regime probability > 60%

No leverage added (TQQQ is already 3x leveraged)

Backtest period: 2015-01-15 to 2025-07-09

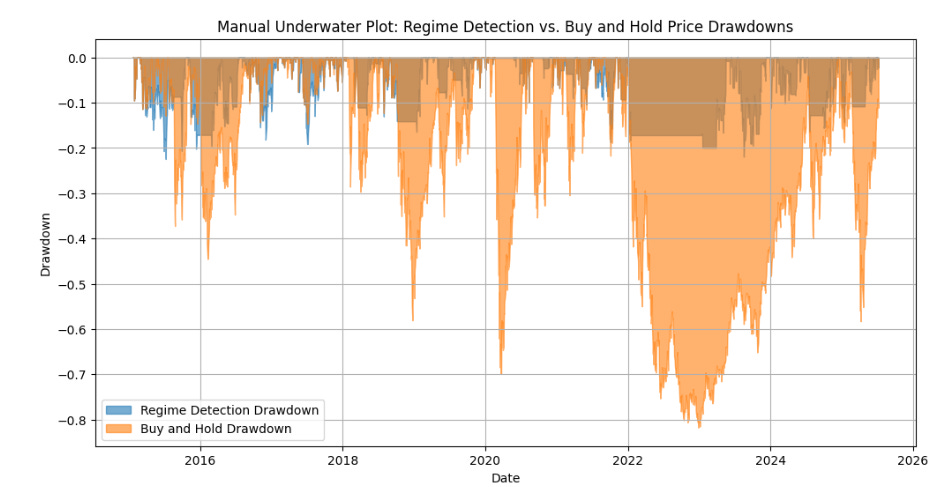

import numpy as np import pandas as pd import yfinance as yf import matplotlib.pyplot as plt # --- Step 1: Fetch price data from Yahoo Finance --- def get_yfinance_data(symbol: str, start: str, end: str) -> pd.DataFrame: df = yf.download(symbol, start=start, end=end, auto_adjust=False) if isinstance(df.columns, pd.MultiIndex): df.columns = ['_'.join(col).strip() if col[1] else col[0] for col in df.columns.values] df = df.reset_index() if 'date' not in df.columns and 'Date' in df.columns: df.rename(columns={'Date': 'date'}, inplace=True) # Try to find the close column smartly (case insensitive) close_col = None for col in df.columns: if col.lower().startswith('close'): close_col = col break if close_col is None: raise KeyError("No 'close' column found in yfinance data!") df = df[['date', close_col]].rename(columns={close_col: 'close'}) df['date'] = pd.to_datetime(df['date']) return df # --- Step 2: Backtest using HMM signal --- def backtest_from_signal(signal_df: pd.DataFrame, price_df: pd.DataFrame, transaction_cost: float = 0.001) -> pd.DataFrame: # Reset MultiIndex if present if isinstance(signal_df.index, pd.MultiIndex): signal_df = signal_df.reset_index() if isinstance(price_df.index, pd.MultiIndex): price_df = price_df.reset_index() # Ensure 'date' is a datetime column with no timezone signal_df['date'] = pd.to_datetime(signal_df['date']).dt.tz_localize(None) price_df['date'] = pd.to_datetime(price_df['date']).dt.tz_localize(None) # Now merge on 'date' df = pd.merge(price_df, signal_df[['date', 'signal']], on='date', how='inner') df['log_return'] = np.log(df['close'] / df['close'].shift(1)) df.dropna(inplace=True) df['signal'] = df['signal'].shift(1).fillna(0) df['position'] = np.where(df['signal'] > 0.6, 1, 0) df['strategy_return'] = df['position'] * df['log_return'] df['trade'] = df['position'].diff().abs().fillna(0) df['strategy_return_net'] = df['strategy_return'] - df['trade'] * transaction_cost df['equity'] = np.exp(df['strategy_return_net'].cumsum()) return df[['date', 'close', 'signal', 'position', 'log_return', 'strategy_return_net', 'equity']] # --- Step 3: Plot the equity curve and closing price --- def plot_equity(df: pd.DataFrame): fig, ax = plt.subplots(figsize=(12, 6)) df['equity_pct'] = (df['equity'] / df['equity'].iloc[0] - 1) * 100 df['close_pct'] = (df['close'] / df['close'].iloc[0] - 1) * 100 ax.plot(df['date'], df['equity_pct'], label='Regime Detection TQQQ pct (% Return)', color='blue') ax.plot(df['date'], df['close_pct'], label='Buy and Hold TQQQ pct (% Return)', color='green', alpha=0.6) ax.set_xlabel("Date") ax.set_ylabel("Return (%) from Start") ax.grid(True) ax.legend(loc="upper left") plt.title("Regime Detection vs Buy and Hold (% Return from Starting Point)") plt.tight_layout() plt.show() # --- Step 4: Drawdown calculation --- def calculate_drawdown(returns): cumulative_returns = (1 + returns).cumprod() peak = cumulative_returns.expanding(min_periods=1).max() drawdown = (cumulative_returns / peak) - 1 return drawdown def plot_underwater(strategy_df: pd.DataFrame): if 'date' in strategy_df.columns: strategy_df['date'] = pd.to_datetime(strategy_df['date']) strategy_df = strategy_df.set_index('date') elif not isinstance(strategy_df.index, pd.DatetimeIndex): print("Warning: DataFrame index is not datetime. Attempting to convert.") strategy_df.index = pd.to_datetime(strategy_df.index) equity_returns = strategy_df['equity'].pct_change().dropna() close_returns = strategy_df['close'].pct_change().dropna() equity_drawdown = calculate_drawdown(equity_returns) close_drawdown = calculate_drawdown(close_returns) fig, ax = plt.subplots(figsize=(12, 6)) ax.fill_between(equity_drawdown.index, equity_drawdown, 0, color='tab:blue', alpha=0.6, label='Regime Detection Drawdown') ax.fill_between(close_drawdown.index, close_drawdown, 0, color='tab:orange', alpha=0.6, label='Buy and Hold Drawdown') plt.title("Manual Underwater Plot: Regime Detection vs. Buy and Hold Price Drawdowns") plt.xlabel("Date") plt.ylabel("Drawdown") plt.grid(True) plt.legend() plt.show() # --- Step 5: Run the backtest pipeline using yfinance --- def run_pipeline(signal_df: pd.DataFrame, symbol: str, start: str, end: str): # Flatten signal_df index if needed if isinstance(signal_df.index, pd.MultiIndex): signal_df = signal_df.reset_index() price_df = get_yfinance_data(symbol, start, end) equity_df = backtest_from_signal(signal_df, price_df) plot_equity(equity_df) plot_underwater(equity_df) final_equity = equity_df['equity'].iloc[-1] total_return = final_equity / equity_df['equity'].iloc[0] - 1 print(f"✅ Final equity: {final_equity:.2f} | Total return: {total_return:.2%}") return equity_df

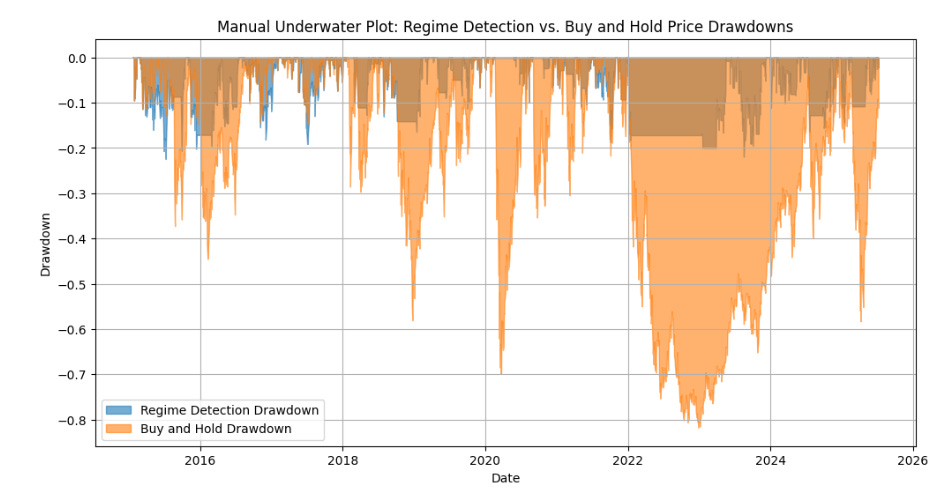

📉 Dramatic Drawdown Reduction

One of the key benefits wasn’t just return — it was risk reduction:

✅ Drawdowns are significantly lower than buy-and-hold TQQQ

✅ The strategy exits during weak regimes, avoiding major crashes

✅ Equity curve is smoother and more compounding-friendly

We visualized this in a custom underwater plot to compare strategy vs. passive investing — the difference is stark.

🛑 Important Disclaimer

⚠️ Backtested results are not guarantees of future performance. This strategy uses historical data and should be viewed as a research demonstration only. Leveraged ETFs like TQQQ are inherently risky and may not be suitable for all investors. Always do your own due diligence and consider speaking with a financial advisor.

✅ Why Now Is the Perfect Moment to Subscribe

You’ve just seen impressive historical results, including:

Annual return of 62.98% (based on backtested data)

Sharpe ratio of 1.74 (indicating strong risk-adjusted performance)

Max drawdown limited to -22.44%

Cumulative returns of over 16,000% across the backtest period

While past performance is not a guarantee of future results, these metrics highlight the potential value of quantitative regime detection strategies.

This is a great opportunity to stay informed and deepen your understanding of these approaches.

🔥 What You’ll Receive When You Subscribe

Early access to new strategy backtests and research, delivered before public release

Educational content on advanced quant models and market regime insights

Thoughtful analysis designed to help you better understand risk and opportunity

Updates on new tools and APIs to support your quant trading journey

📩 Interested in receiving actionable quant insights?

👉 Subscribe to the free QuantHQ Newsletter and get fresh analysis and strategy ideas delivered directly to your inbox.

Please remember: This newsletter is for educational purposes only and does not constitute financial advice or an offer to trade securities.